Betfair Help

Commissions and Charges

Betfair Commission is the only charge that most customers on Betfair will ever have to pay.

Each market that you bet on has a Market Base Rate (MBR). This rate is the maximum percentage of your winnings that you will pay in commission. To find out what the Market Base Rate is for a market, click on the “Rules” section of the Market you wish to place a bet on to find it. Betfair Commission is automatically removed from your winnings when the market is settled.

BETFAIR COMMISSION EXAMPLE

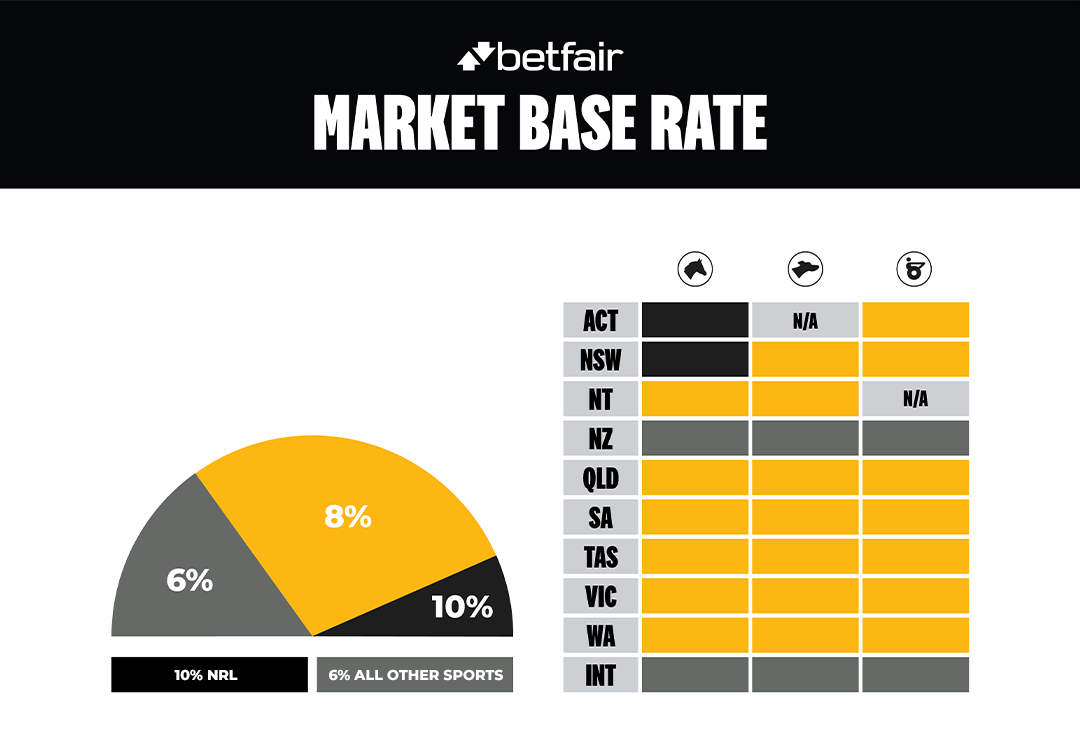

For example, Victorian thoroughbred racing (i.e. the Melbourne Cup market) has a 8% Market Base Rate.

You place a $50 BACK bet on Incentivise in the Melbourne Cup at odds of $3.00. Incentivise wins. This means that your winnings are $100 ($150 return – $50 stake).

With the Market Base Rate at 8%, the commission you will pay is $100 x 8% = $8.00.

WHAT ARE THE MARKET BASE RATES?

Market Base Rates for sport and international racing markets are 6%, except for NRL at 10%. On Australian racing markets, the Market Base Rate is either 8% or 10%, depending on the state and racing code. These variable Market Base Rates reflect the product fees each racing and sporting body charges Betfair. Please refer to the image below to find exactly what rate is charged.

OTHER CHARGES

Some customers may incur other types of charges through extremely high activity on the Betfair Exchange. Most Betfair customers will never encounter these charges. To find out more about these charges, please click on the relevant links below:

Premium Charges

Transaction Charges

Turnover Charge

Want to get answers to your questions?

Go To Betfair FAQs